First published by our media partner FinDev Gateway who, in the run-up to European Microfinance Week, are highlighting some of fascinating topics and sesion to be covered during #enw2019.

The promise of financial inclusion is very attractive: creating positive change in clients' lives while making a financial return. But what evidence do we have that the financial inclusion industry is achieving those goals? And how do we know if a particular result – such as 30% female borrowers, or 5% ROE (return on equity) or a 60 transparency index – is good or bad? Also, is it possible for social returns to weigh as much as financial returns in decision-making? And how do we manage the sensitive topic of pricing?

The promise of financial inclusion is very attractive: creating positive change in clients' lives while making a financial return. But what evidence do we have that the financial inclusion industry is achieving those goals? And how do we know if a particular result – such as 30% female borrowers, or 5% ROE (return on equity) or a 60 transparency index – is good or bad? Also, is it possible for social returns to weigh as much as financial returns in decision-making? And how do we manage the sensitive topic of pricing?

All of these big questions point us to the reasons that data and benchmarks are so needed. Facts and figures tell us the full story of financial and social results and allow us to assess that story compared to the stories of peers. But after MicroFinance Transparency closed, and with MIX Market no longer collecting microfinance data, access to data and benchmarks about financial services providers (FSPs) has become more difficult. Still, there is an ongoing need for financial inclusion data. This is how the idea for the ATLAS data platform came about.

What is ATLAS?

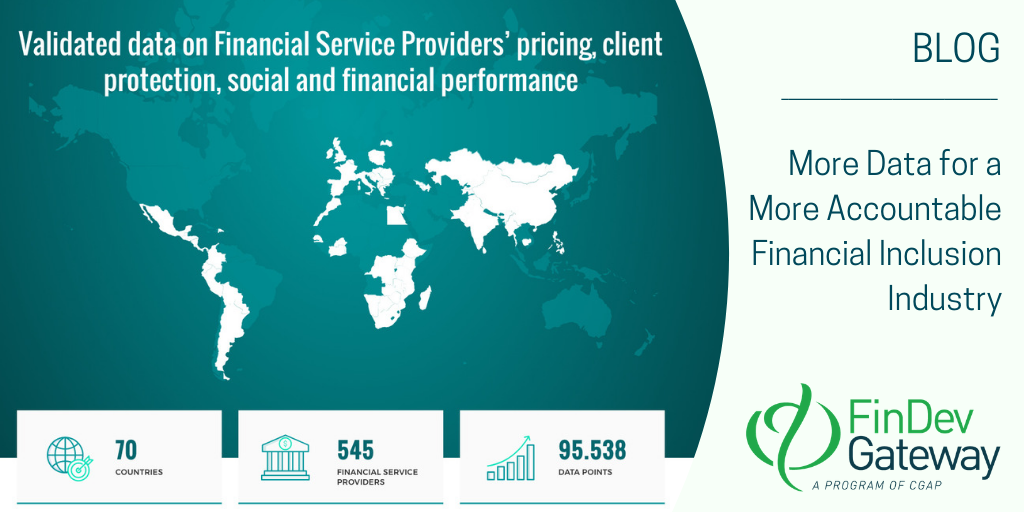

ATLAS is an online platform which centralizes FSP data on pricing, client protection, social and financial performance, and helps to make our industry accountable through reporting, benchmarking, and data consolidation. FSP data is provided on an ongoing basis by a variety of sources, including the FSPs themselves, MFR, CERISE, the Smart Campaign, networks, associations, investors, and other rating agencies willing to join. We ensure the reliability of data through a score based on the consistency and degree of external validation received such as ratings and certifications, which increase the average reliability of data. Moreover, the ATLAS database includes the MicroFinance Transparency pricing data and it will soon include the MIX publicly available data.

A variety of different tools are available for data providers to report to ATLAS, and they can decide to share their data with subscribers in a nominative or anonymous manner. In return for reporting to ATLAS, data providers gain international visibility, a Price Disclosure Award and free access to a general benchmark.

How does it work?

ATLAS data will be offered through subscription to different types of plans starting in early 2020. We aim to provide a permanent home for this data by building a sustainable business model for the new data platform. Sustainability is a key priority for us at MFR, and we have strong experience with remaining sustainable in the face of major business changes. After the microfinance rating funds closed ten years ago, we streamlined our processes and listened to the market to diversify, and in this way we were able to stay in business and grow. Our business model for ATLAS keeps sustainability at the forefront by:

- Integrating the notion of subscription for access from the very beginning.

- Maximizing efficiency by having an existing organization with built-in capacity run the initiative (MFR).

- Relying on a substantial amount of high-quality data already available from MFR's core business as a rating agency.

All that said, ATLAS would not exist without the support of ATLAS sponsors. However, the ATLAS business model only includes initial subsidies in relatively small amounts. These subsidies are not part of the long-term model, but strategically placed to cover the initial costs of the project until the subscription uptake is sufficient to cover the full costs.

Who should use this platform, and for what?

ATLAS is meant to be used by all the different stakeholders in the microfinance sector – including investors, international networks, FSPs, professional associations, standard-setting bodies and researchers.

Investors and international networks can use the new platform to screen, benchmark, monitor and aggregate their portfolios. They can review market trends in countries and regions before investing, benchmarking their investee to strengthen the due diligence process (e.g. on pricing). By requesting that their investees report on ATLAS, and by defining their covenants on their ATLAS profile, investors can easily monitor their investees' performance trends and compliance with the covenants.

The same can be done by international networks, who can use ATLAS to consolidate the individual data of their affiliates in one aggregate performance report. From an industry perspective, it is more efficient to share a common system and pay for this infrastructure once, instead of having each investor and international network develop individual systems.

FSPs can simplify their reporting to different stakeholders by using ATLAS as a common platform. FSPs sometimes have up to 30 different quarterly reports to fill out for investors and other external parties, a process which could be made much more efficient. By partnering with investors that use ATLAS to manage their portfolio, FSPs can fill out one ATLAS report containing their investors' fields of interest, and thus fulfil their reporting duty to multiple investors.

Professional associations who have a clear understanding of their country or region can use ATLAS to add value to their members by benchmarking their trends. ATLAS allows them to consolidate data and compare their performance to regional or global standards. By partnering with ATLAS, associations also gain international visibility and benefit from exposure to free materials and trainings, such as on APR calculation.

The ATLAS data platform can also provide the data evidence that Standard Setting Bodies (SSBs) need in order to develop effective standards. And finally, researchers can study the industry evolution, drivers, and relations based on a reliable and diversified database.

Who's behind this new effort to consolidate microfinance data?

ATLAS is managed by the rating agency MFR under the governance of the sponsoring organizations: Agence Française de Développement (AFD), Proparco, ADA, Luxembourg Aid and Development, Liechtenstein Development Initiative, CDC, and Swedish International Development Cooperation Agency (SIDA).

Partner organizations include CERISE, the Smart Campaign, the Social Performance Task Force (SPTF), Microfact, MIMOSA, Poverty Probability Index (PPI), and Microfinance Transparency.

Any initiative that shares the goal of responsible finance is welcome to join. For more information, please contact Lucia Spaggiari: l.spaggiari@mf-rating.com

First published by our media partner FinDev Gateway who, in the run-up to European Microfinance Week, are highlighting some of fascinating topics and sesion to be covered during #enw2019.

All of these big questions point us to the reasons that data and benchmarks are so needed. Facts and figures tell us the full story of financial and social results and allow us to assess that story compared to the stories of peers. But after MicroFinance Transparency closed, and with MIX Market no longer collecting microfinance data, access to data and benchmarks about financial services providers (FSPs) has become more difficult. Still, there is an ongoing need for financial inclusion data. This is how the idea for the ATLAS data platform came about.

What is ATLAS?

ATLAS is an online platform which centralizes FSP data on pricing, client protection, social and financial performance, and helps to make our industry accountable through reporting, benchmarking, and data consolidation. FSP data is provided on an ongoing basis by a variety of sources, including the FSPs themselves, MFR, CERISE, the Smart Campaign, networks, associations, investors, and other rating agencies willing to join. We ensure the reliability of data through a score based on the consistency and degree of external validation received such as ratings and certifications, which increase the average reliability of data. Moreover, the ATLAS database includes the MicroFinance Transparency pricing data and it will soon include the MIX publicly available data.

A variety of different tools are available for data providers to report to ATLAS, and they can decide to share their data with subscribers in a nominative or anonymous manner. In return for reporting to ATLAS, data providers gain international visibility, a Price Disclosure Award and free access to a general benchmark.

How does it work?

ATLAS data will be offered through subscription to different types of plans starting in early 2020. We aim to provide a permanent home for this data by building a sustainable business model for the new data platform. Sustainability is a key priority for us at MFR, and we have strong experience with remaining sustainable in the face of major business changes. After the microfinance rating funds closed ten years ago, we streamlined our processes and listened to the market to diversify, and in this way we were able to stay in business and grow. Our business model for ATLAS keeps sustainability at the forefront by:

All that said, ATLAS would not exist without the support of ATLAS sponsors. However, the ATLAS business model only includes initial subsidies in relatively small amounts. These subsidies are not part of the long-term model, but strategically placed to cover the initial costs of the project until the subscription uptake is sufficient to cover the full costs.

Who should use this platform, and for what?

ATLAS is meant to be used by all the different stakeholders in the microfinance sector – including investors, international networks, FSPs, professional associations, standard-setting bodies and researchers.

Investors and international networks can use the new platform to screen, benchmark, monitor and aggregate their portfolios. They can review market trends in countries and regions before investing, benchmarking their investee to strengthen the due diligence process (e.g. on pricing). By requesting that their investees report on ATLAS, and by defining their covenants on their ATLAS profile, investors can easily monitor their investees' performance trends and compliance with the covenants.

The same can be done by international networks, who can use ATLAS to consolidate the individual data of their affiliates in one aggregate performance report. From an industry perspective, it is more efficient to share a common system and pay for this infrastructure once, instead of having each investor and international network develop individual systems.

FSPs can simplify their reporting to different stakeholders by using ATLAS as a common platform. FSPs sometimes have up to 30 different quarterly reports to fill out for investors and other external parties, a process which could be made much more efficient. By partnering with investors that use ATLAS to manage their portfolio, FSPs can fill out one ATLAS report containing their investors' fields of interest, and thus fulfil their reporting duty to multiple investors.

Professional associations who have a clear understanding of their country or region can use ATLAS to add value to their members by benchmarking their trends. ATLAS allows them to consolidate data and compare their performance to regional or global standards. By partnering with ATLAS, associations also gain international visibility and benefit from exposure to free materials and trainings, such as on APR calculation.

The ATLAS data platform can also provide the data evidence that Standard Setting Bodies (SSBs) need in order to develop effective standards. And finally, researchers can study the industry evolution, drivers, and relations based on a reliable and diversified database.

Who's behind this new effort to consolidate microfinance data?

ATLAS is managed by the rating agency MFR under the governance of the sponsoring organizations: Agence Française de Développement (AFD), Proparco, ADA, Luxembourg Aid and Development, Liechtenstein Development Initiative, CDC, and Swedish International Development Cooperation Agency (SIDA).

Partner organizations include CERISE, the Smart Campaign, the Social Performance Task Force (SPTF), Microfact, MIMOSA, Poverty Probability Index (PPI), and Microfinance Transparency.

Any initiative that shares the goal of responsible finance is welcome to join. For more information, please contact Lucia Spaggiari: l.spaggiari@mf-rating.com