For its annual meeting in Luxembourg this year, CGAP asked e-MFP to organize a session for its members. This was our first opportunity to present some of the lessons being highlighted by the 7th European Microfinance Award “Microfinance and Access to Education”, especially the role that donors and investors can play to support the efforts of MFIs to promote access to quality education at the bottom of the pyramid.

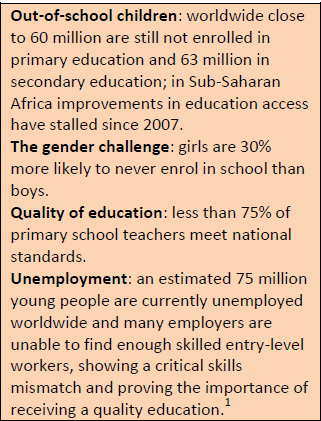

Francesca Agnello, consultant supporting the 7th European Microfinance Award, set the scene by pointing out that finding ways to deliver and promote access to quality education is one of the great challenges of our time. Though the primary completion rate in developing countries reached 91% in 2013, an impressive increase of 12 points since 1990, other indicators (such as number out-of-school children, gender, quality of education or youth unemployment) show that there is still plenty to do if we want to achieve the targets of SDG4 “Ensure inclusive and equitable quality education and promote lifelong learning opportunities for all” by 2030.

Francesca Agnello, consultant supporting the 7th European Microfinance Award, set the scene by pointing out that finding ways to deliver and promote access to quality education is one of the great challenges of our time. Though the primary completion rate in developing countries reached 91% in 2013, an impressive increase of 12 points since 1990, other indicators (such as number out-of-school children, gender, quality of education or youth unemployment) show that there is still plenty to do if we want to achieve the targets of SDG4 “Ensure inclusive and equitable quality education and promote lifelong learning opportunities for all” by 2030.

Financial barriers are a major cause of inadequate access to education, affecting both the supply and demand sides of the sector. On the supply side, insufficient public funding results in quantity and quality shortages (lack of schools, teachers, equipment and good teaching practices) that lead to reliance on private schools to be able to respond to the demand. And if meeting the costs of public education (uniforms, supplies, transport, etc.) can be a struggle for poor families, paying private school fees is an even greater challenge. Effective financial services can thus meet key needs of both the schools themselves and of the families and students that attend them.

MFIs are well placed to deal with both sides of the sector: their MSME products can well serve the needs of low cost schools, which are themselves small businesses; and they are almost by definition set up to respond to the financial needs of poor households. Francesca described how MFIs provide financial and non-financial services to schools and families and students: the former can access education provider loans as well as capacity building services often coupled with these loans, while the latter can be offered a wide array of financial services (loans, savings, insurance and remittances) to cover education needs. Some MFIs may also provide education-to-employment programs for youth and unemployed adults, either directly or through affiliated partners.

MFIs are not the only player that can have a say on educational finance for the bottom of the pyramid; other stakeholders can play a key role in supporting the MFIs’ efforts and initiatives. The session featured two case studies of investment funds active in this field, the Higher Education Finance Fund (HEFF) and the Regional Education Finance Fund for Africa (REFFA), as well as the experience of the MasterCard Foundation.

The Higher Education Finance Fund (HEFF) was launched in 2011 in order to finance higher education through MFIs for the poor in Latin America, where the cost of tertiary education has risen dramatically in recent years and the financing instruments, when they exist, are not sufficient or sustainable and in some cases benefit more middle and lower middle income students.

Kaspar Wansleben, Executive Director of the Luxembourg Microfinance Development Fund (LMDF) and member of HEFF Board, explained how HEFF provides MFIs with not only funding, but also technical assistance so that they are able to offer loans for higher education with terms that are affordable to low income students who otherwise wouldn’t have the means to pay for their education. The US$34 million fund is financing 10 MFIs in seven countries: Guatemala, Honduras, Costa Rica, Dominican Republic, Bolivia, Peru and Paraguay. Technical assistance (US$ 1.6 million) is used for market analysis, including identifying a roster of quality education providers and highly-demanded careers that would allow students to use a reasonable portion of their subsequent salary to repay their loans after graduation. Technical assistance has also enabled the MFIs to make the necessary internal and system changes to support these education loans, as well as support student mentoring and counselling.

Kaspar Wansleben, Executive Director of the Luxembourg Microfinance Development Fund (LMDF) and member of HEFF Board, explained how HEFF provides MFIs with not only funding, but also technical assistance so that they are able to offer loans for higher education with terms that are affordable to low income students who otherwise wouldn’t have the means to pay for their education. The US$34 million fund is financing 10 MFIs in seven countries: Guatemala, Honduras, Costa Rica, Dominican Republic, Bolivia, Peru and Paraguay. Technical assistance (US$ 1.6 million) is used for market analysis, including identifying a roster of quality education providers and highly-demanded careers that would allow students to use a reasonable portion of their subsequent salary to repay their loans after graduation. Technical assistance has also enabled the MFIs to make the necessary internal and system changes to support these education loans, as well as support student mentoring and counselling.

HEFF aims to demonstrate that with the right methodologies and principles, student lending can be done on a sustainable basis by a private for-profit financial intermediary and in this regard they consider MFIs the ideal vehicle due to their proven capacity to manage sustainable lending programmes and reach households in marginal urban areas and rural settings with products adapted to their needs. Though HEFF is only now seeing the first batch of graduates emerge from its programme, the early figures are promising. As of 31st December 2015 the fund has reached a total of 2,667 students, 70% of whom under 25 years old and 57% from families with an average income below US$730 per month. Most students also combine their studies with work.

While HEFF focuses on student finance, the Regional Education Finance Fund for Africa (REFFA) provides funding for both students and education providers. Maria Teresa Zappia, CIO of BlueOrchard, REFFA’s fund manager, referred to a recent study that found that almost 25% of primary students in poor countries are enrolled in private schools.[2] This is especially a growing reality in Africa, where public education has simply been unable to cope with the growing demand due to population growth and increased emphasis on education; meaning also that teaching quality has not kept up. For example, in Tanzania, there is one trained teacher for every 100 students. Consequentially it produces a particular challenge for poor families that sometimes spend 40% to 50% of their income on education.

In this context, REFFA was launched in 2012 with the overall objective of increasing equal access to secondary, vocational and higher education, and enhancing quality of education. The US$27 million fund provides loans and technical assistance to MFIs that offer customized loans to schools, as well as education loans and savings products to families and students. Currently the fund is working in 6 countries: Cameroon, Dem. Republic of Congo (DRC), Ghana, Kenya, Senegal, and Tanzania.

Maria Teresa focused especially on working with schools to raise the quality of education. She presented the results of a survey of educational providers financed by ProCredit Bank in DRC, which found that this funding has allowed the schools to increase enrolment by an average of 220 students per loan cycle, improve their infrastructure, hire 2 to 8 more staff and increase staff wages. An interesting finding was that, while 80% of the schools had increased their operating profit after receiving the loan, their profitability ratios fell due to the fact that school owners decided to invest in the school, sacrificing higher profits in the short-term to insure the long-term success of their schools.

REFFA plans to expand to 11 countries in 2016 and its next steps include piloting education quality measurement tools; defining criteria for affordable schools to be used by the MFIs; and continuing to improve the relevance of the technical assistance provided to the MFIs while at the same time combining it with technical assistance to support education service providers such as schools, school associations, the government agencies, and others.

The last speaker to take the floor was Mark Wensley, Senior Program Manager, Financial Inclusion at the MasterCard Foundation. As a donor, the Foundation is promoting and supporting education finance through several partnerships and projects. Mark highlighted in particular the Foundation’s partnership with Opportunity International to provide education finance tools that allow children to access a quality education in rural settings. These tools include education-focused loans, savings and insurance, not only to allow parents to send their children to school and support schools, but also ensure that children will be able to continue to go to school if something happens to their parents. The programme started in December 2013 and is deployed in six countries: Ghana, Kenya, Malawi, Rwanda, Uganda and Tanzania.

Mark also mentioned the Youth Employment Initiative launched by the Foundation in December 2015 to train and help transition 200,000 out-of-schools and unemployed youth in Ghana and Uganda into sustainable jobs in the construction and agricultural sectors. The initiative includes training for skills development, networking opportunities and access to appropriate financial services to further their education, support their job search or help them start their own business.

As Francesca said at the beginning, providing access to quality education is a huge challenge; but as subsequent speakers pointed out, MFIs and their partners are beginning to address the issue with real-world solutions. As the 7th European Microfinance Award gets underway, we hope to see many more such examples. Don’t forget the deadline for applications is June 1st!

About the Award

First held in 2006 and jointly organised by the Luxembourg Ministry of Foreign and European Affairs, e-MFP and the Inclusive Finance Network Luxembourg (InFiNe.lu), the European Microfinance Award includes a prize of €100.000 to be awarded on November 17th 2016 during the European Microfinance Week, at a ceremony to which the three finalists will be invited and will present a short video about their programs. For more information, visit: www.european-microfinance-award.com

[1] Education to employment: Designing a system that works, McKinsey Center for Government, 2013. http://mckinseyonsociety.com/downloads/reports/Education/Education-to-Employment_FINAL.pdf

Leave a comment