The third in a series of blog contributions throughout this year to complement the European Microfinance Award 2021 on ‘Inclusive Finance and Health Care’, Shams Azad and Rubait Jannat from BRAC Microfinance examine the rationale for medical loans, with a particular focus on BRAC’s MTL+ product. Over the coming months, we’ll be publishing more in this series from our members and other experts in the field. Watch this space!

The need for client-centric financing during an emergency

Bangladesh has recorded notable achievements in the healthcare sector in the last few decades. Reforms and a drive to develop an extensive healthcare infrastructure have led to reduced child and maternal mortality rates, increased immunisation, and progress in combating infectious diseases like malaria and tuberculosis. All of these achievements are remarkable among south Asian nations. But still, an all-inclusive health care system is a far-reaching goal.

An estimated 67% of total healthcare expenditure is met from households’ out-of-pocket (OOP) expenses, one of the highest in the South-East Asia region. Out of this OOP expenditure, 69.4% goes on medicines, exacerbated by the absence of a national health insurance system. So low-income households experience different and serious vulnerabilities during health emergencies.

Nearly 5 million people are pushed below the poverty line due to health-related catastrophes every year. Institutional financing options are limited. Accessing a regular microfinance loan also takes 3 to 4 days. And so in most cases, borrowing from friends or relatives or informal sources at higher rates or selling assets are the natural response to a unforeseen health expenses. Because of these factors, there is a real need to create a client-centric financing option for low-income families to tackle a medical emergency. In response to this need, BRAC Microfinance in Bangladesh launched "Medical Treatment Loan (MTL)" back in 2013.

Shielding people from health shocks: Medical treatment loans

The MTL helps families to respond to unprecedented medical expenditures and provides linkages with hospitals and clinics. The core initial consideration was: how can a field officer be involved in the household's decision-making process in a time of medical emergency to ensure there is no ‘purpose drift’ and the intervention does not lead to over-indebtedness. Clients were matched with a BRAC-doctor, and the loan amount considered per the doctor's recommendation, within a range from USD50 to 600, parameters decided based on market experience. If the required amount was more than USD 235, disbursement was in two phases. As the MTL was offered only to existing borrowers and/or savings, it was expected that the MTL would be taken as a top-up to an existing loan.

Relaunching MTL as MTL+

After several years of improvements and insights from the MTL programme, there was a product re-design. Endorsement from the BRAC-assigned doctor was not always convenient. Travelling long distances to reach the doctor's clinic, especially in rural areas, and the lack of availability of the doctor or appointment clashes led to requests from clients’ families that they could choose the health provider themselves.

Furthermore, the loan cap and two-stage disbursement was not flexible enough for most families. In the three stages of medical recovery - diagnosis, treatment and post-treatment recovery - financing needs might arise anytime. Some treatments, like surgery or childbirth, required money all at once. So fragmented disbursement in those cases was not suitable.

And lastly, the restriction of the loan to existing clients was withdrawn, because a family should be able to start building a financial journey with BRAC even in a time of emergency. BRAC sees this as ‘staying close’ to the people it serves, and for all these reasons, MTL+ was launched in a completely different set of branch offices in 2019.

New lessons learned

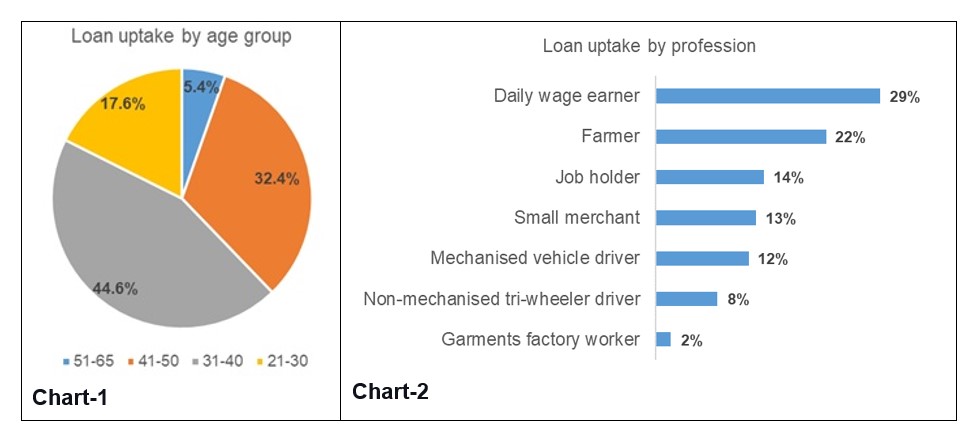

After a year of observations of the new programme, we saw that loan uptake was 10% higher in MTL+ than its predecessor. 75% of the clients were between 31 to 50 years old (chart-1), and by profession, most of the recipient households were in the lower-income bracket – daily earners (chart-2). These households' average per capita income was around the international poverty line of USD1.90 per day, indicating impressive equitable access among the client groups, and that field officers were not just focusing on higher-income households for better repayement. These MTL+ borrowers comprised 3.7% of the total client base, and the average loan amount was USD 150, while the maximum was USD 950. 66% of loans were given for 12 months, 20% for 18 months, and 14% for 24 months.

Lack of awareness or access to finance undoubtedly leads many families to reach out to informal service providers in a country like Bangladesh. Here at BRAC we wanted to learn if an affordable financing option would increase access and uptake of better, formal health care services. From BRAC’s perspective this means visiting a registered physician at any public or private healthcare facility. Our research involved 531 households which had taken the MTL+ loan and 531 households which had not, for similar health cases, and we found that access to such a treatment loan increased the probability of visiting a formal health care service provider by 41%. About 97% of the households from MTL+ clients went to formal healthcare providers for their illnesses, compared to only 61% of non-MTL+ households. MTL+ households also had higher OOP expenditure (USD225) versus non-MTL_ households (USD76), due to the removal of liquidity constraints. We also observed that MTL+ clients spent about USD 93 more on average for their treatment than they did on previous similar health incidents before the loan uptake, however their net expenditure decreased by USD 35.5 on average. These data suggest that MTL+ relaxes the burden on their regular income and household cash savings.

Shahina used to run a small grocery store adjacent to her house, and her husband was a person with a disability. The family expenses were on Shahina's income. When she was once diagnosed with stones in her gallbladder, she was at a loss. Then she availed of BRAC's MTL+, an amount of USD 175 and successfully went through her surgery.

Shahina used to run a small grocery store adjacent to her house, and her husband was a person with a disability. The family expenses were on Shahina's income. When she was once diagnosed with stones in her gallbladder, she was at a loss. Then she availed of BRAC's MTL+, an amount of USD 175 and successfully went through her surgery.

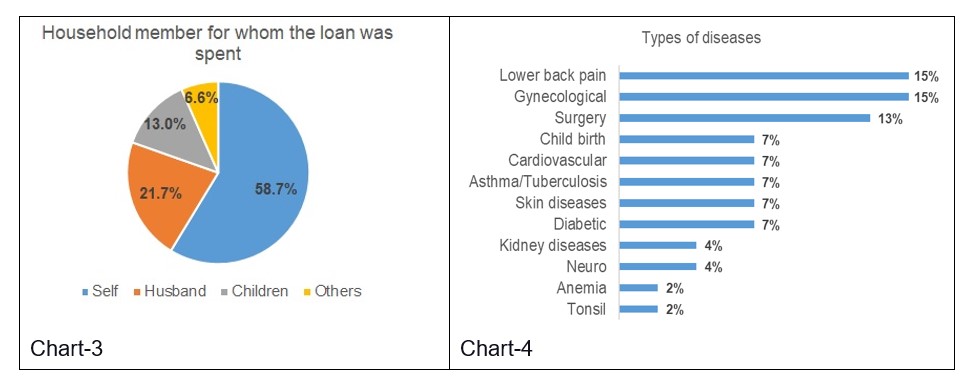

The intervention also has a considerable benefit for women. The MTL+ loan was offered to female client groups and in almost 60% of cases (chart-3) the clients used the loan for their own treatment purpose, with a further 35% of spending on immediate family members, husband or children. The types of illnesses being treated also varied widely (chart-4). Full recovery from the illness was observed in 58.7% of the cases. In 34.8% of the cases, it was partial.

Sultana and her husband, a small business holder, struggled with their son Samiul since his birth due to an "Atrial Septal" defect (a congenital disability of the heart in which there is a hole in the wall divides the upper chambers of the heart). Taking an MTL+ loan of USD 590, the family went through a bypass surgery for Samiul. Today Samiul, aged 7, is fully cured.

Sultana and her husband, a small business holder, struggled with their son Samiul since his birth due to an "Atrial Septal" defect (a congenital disability of the heart in which there is a hole in the wall divides the upper chambers of the heart). Taking an MTL+ loan of USD 590, the family went through a bypass surgery for Samiul. Today Samiul, aged 7, is fully cured.

Of course, an affordable financing option might solve some of issues for low-income households in case of medical emergencies, and MFIs can design an emergency loan, with quick disbursement, without burdensome assessment criteria. However, there are areas of concern. In many cases, clients ask for a grace period on repayment because of the main income earner requires the health treatment, the the monthly repayment load may become unmanageable – especially as 87% of the clients in the BRAC pilot already had a loan before they required the MTL+ top-up.

Does this mean a medical loan should be offered at a subsidised rate? The portfolio quality ratio was higher in MTL+ in comparison to a regular microloan portfolio, but this may not always tell the full story of how families cope, and for an MFI like BRAC it’s a question of balancing repayment ratios with the social mession to ‘stand by’ the households they serve. A simple instrument of loan calculation that uses variables like household income, expenses, debt and savings outstanding, the amount asked for the treatment and proposed loan tenure, can help field officers to take faster decision, and this was implemented in BRAC’s case. The idea is that the field officer can work with the household to evaluate and adjust the variables to create a more bespoke loan that provides a manageable repayment schedule that genuinely helps rather than hurts a family.

Scaling up such a financing option needs more study. What does a low-income household need more- a medical loan or a low cost and effective insurance coverage? Does a financing option make the families incline more towards commercial health care options, thus ending up in higher OOP expenditure? Does the quality of the services worth spending the money on? Moreover, the COVID-19 pandemic has put experimentation at an unprecedented standstill. However, at BRAC we are hopeful of being an important part of the discussion on affordable health care services for low-income households with the experience we are gathering from this medical treatment loan.

Leave a comment